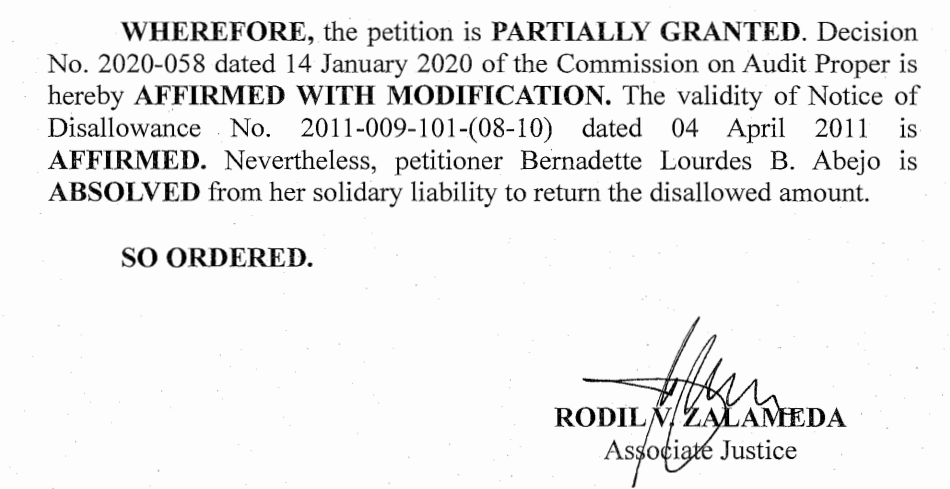

DISPOSITIVE:

SUBJECTS/DOCTRINES/DIGEST:

WHAT HAPPENED IN THIS CASE?

PETITIONER WAS ABSOLVED OF HER SOLIDARY LIABILITY TO RETURN THE DISALLOWED AMOUNT BECAUSE SHE DID NOT ACT IN BAD FAITH. THOSE THAT SHOULD BE HELD LIABLE MUST HAVE ACTED IN EVIDENT BAD FAITH, WITH MALICE, OR THEY WERE GROSSLY NEGLIGENT IN THE PERFORMANCE OF THEIR OFFICIAL DUTIES.

Madera also added that these badges of good faith should be considered first before holding these officers, whose participation in the disallowed transaction was in the performance of their official duties, liable; and that the presence of any of these factors in a case may tend to uphold the presumption of good faith in the performance of official functions accorded to the officers involved.33 Badges of good faith could be appreciated in favor of petitioner. No prior disallowance of the same benefit has been issued against ICAB. Also, there is no precedent disallowing a similar case in jurisprudence. As a matter of fact, the only other COA disallowance petition involving ICAB was a case also entitledAbejo v. Commission on Audit, and docketed as G.R. No. 254570. Said case was resolved by the Court on 29 January 2021, and it pertains to an entirely different incentive. Considering the foregoing, the Court chooses to uphold petitioner’s presumption of good faith.

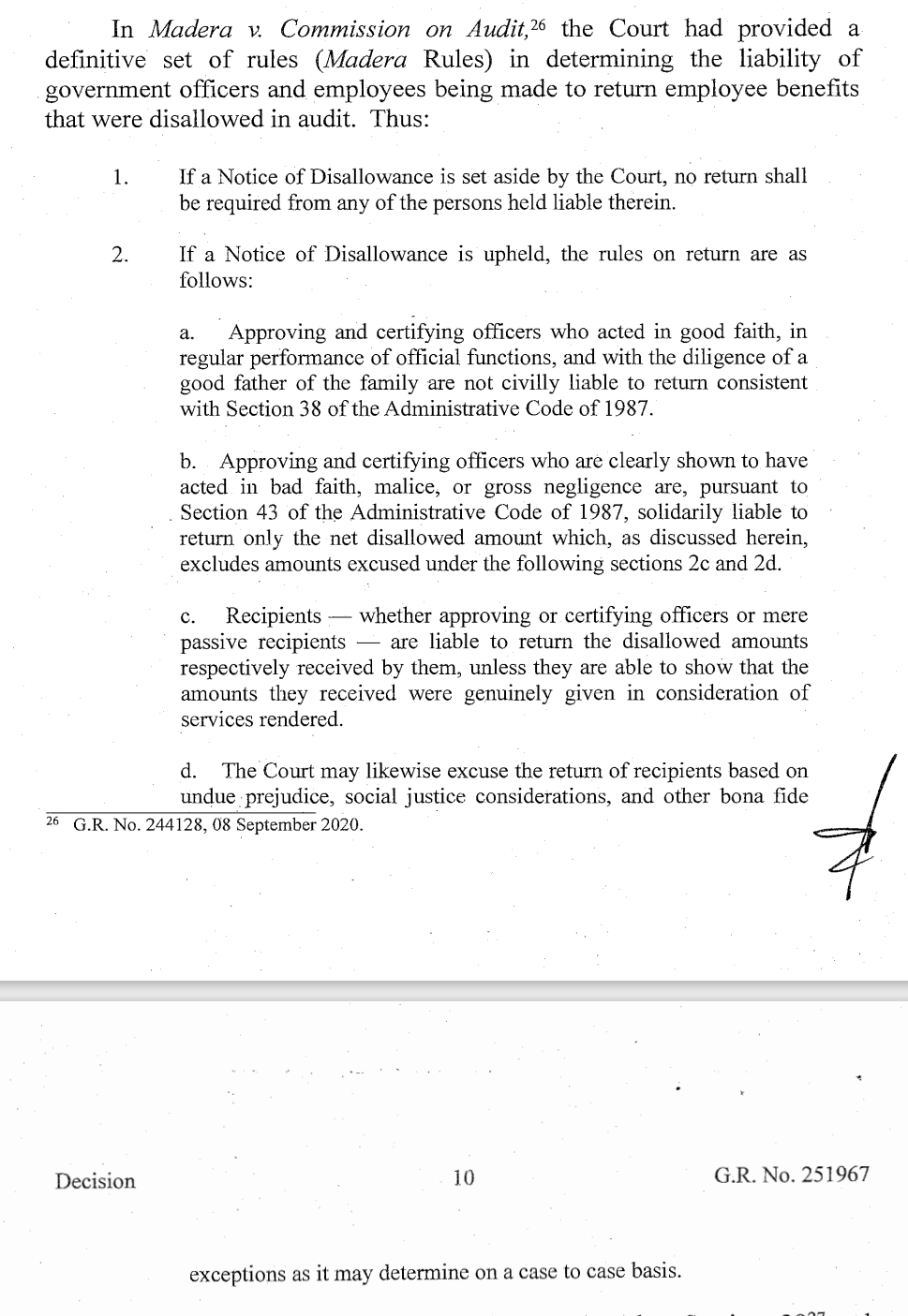

WHAT ARE THE RULES ON EXEMPTING GOVT OFFICIALS FROM RETURNING EMPLOYEE BENEFITS DISALLOWED IN AUDIT?

TO READ THE DECISION, JUST CLICK/DOWNLOAD THE FILE BELOW. IF FILE DOES NOT APPEAR ON SCREEN GO TO DOWNLOAD. IT IS THE FIRST ITEM. OPEN IT.

NOTE: TO RESEARCH ON A TOPIC IN YAHOO OR GOOGLE SEARCH JUST TYPE “attybulao and the topic”. EXAMPLE: TO RESEARCH ON FORUM SHOPPING JUST TYPE “attybulao and forum shopping”.