For legal forms (e.g. deed of sale, affidavit of loss, etc.) you may visit our new website: www.jabbforms.com. You may research on any topic: non-forum shopping, judicial courtesy, etc. by typing on the search box and pressing SEARCH beside the box. For any query email us at attybulao@gmail.com or send text to 09158773983. If you have benefited from this website and you want to donate for its upkeep you may remit to gcash 09158773983 and send us text message. Thank you.

Hey there! Thanks for dropping by J.A.B. Bulao & Associates! Take a look around and grab the RSS feed to stay updated. See you around!

NOTE: TO RESEARCH ON A TOPIC IN YAHOO OR GOOGLE SEARCH JUST TYPE “attybulao and the topic”. EXAMPLE: TO RESEARCH ON FORUM SHOPPING JUST TYPE “attybulao and forum shopping”.

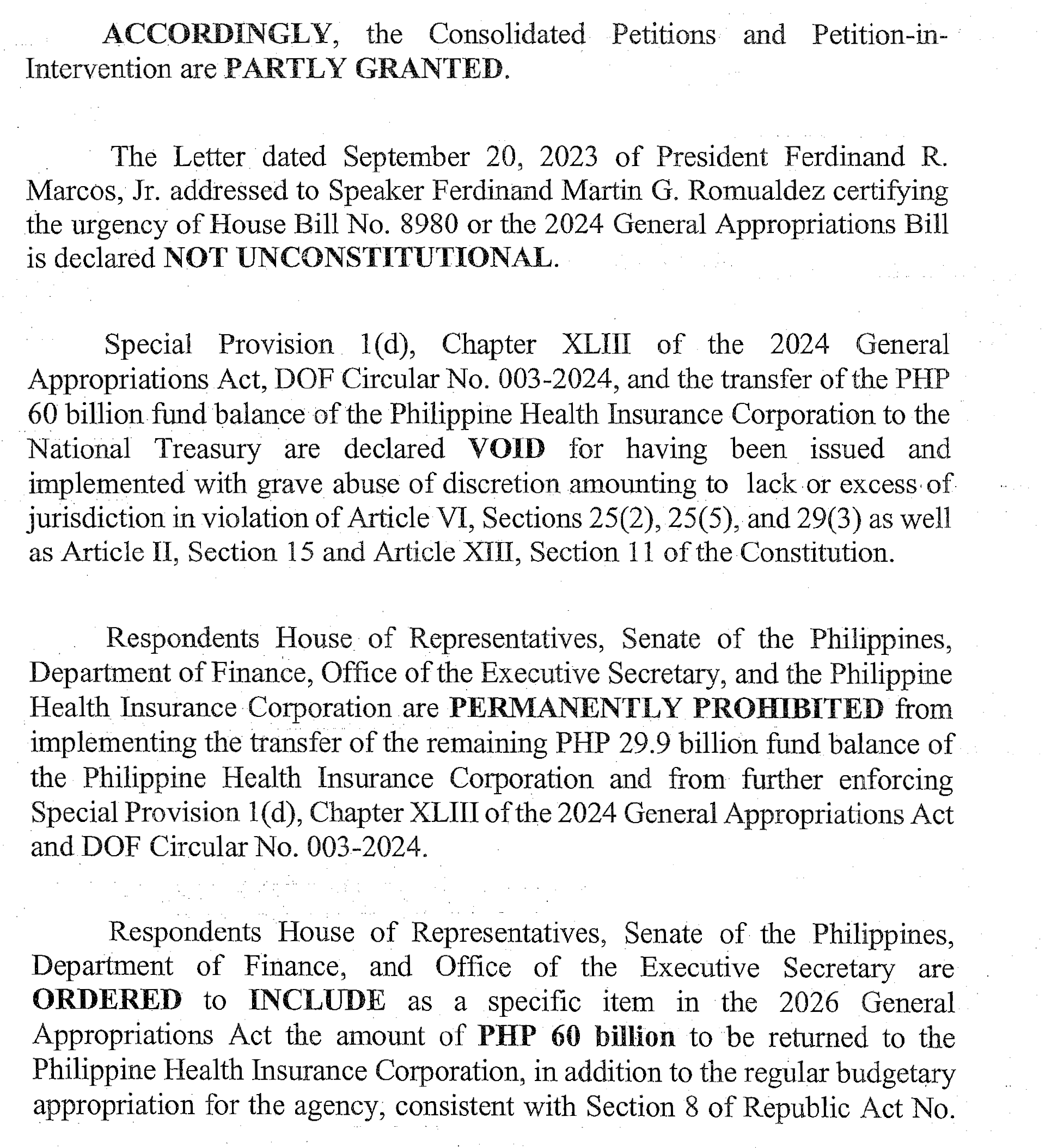

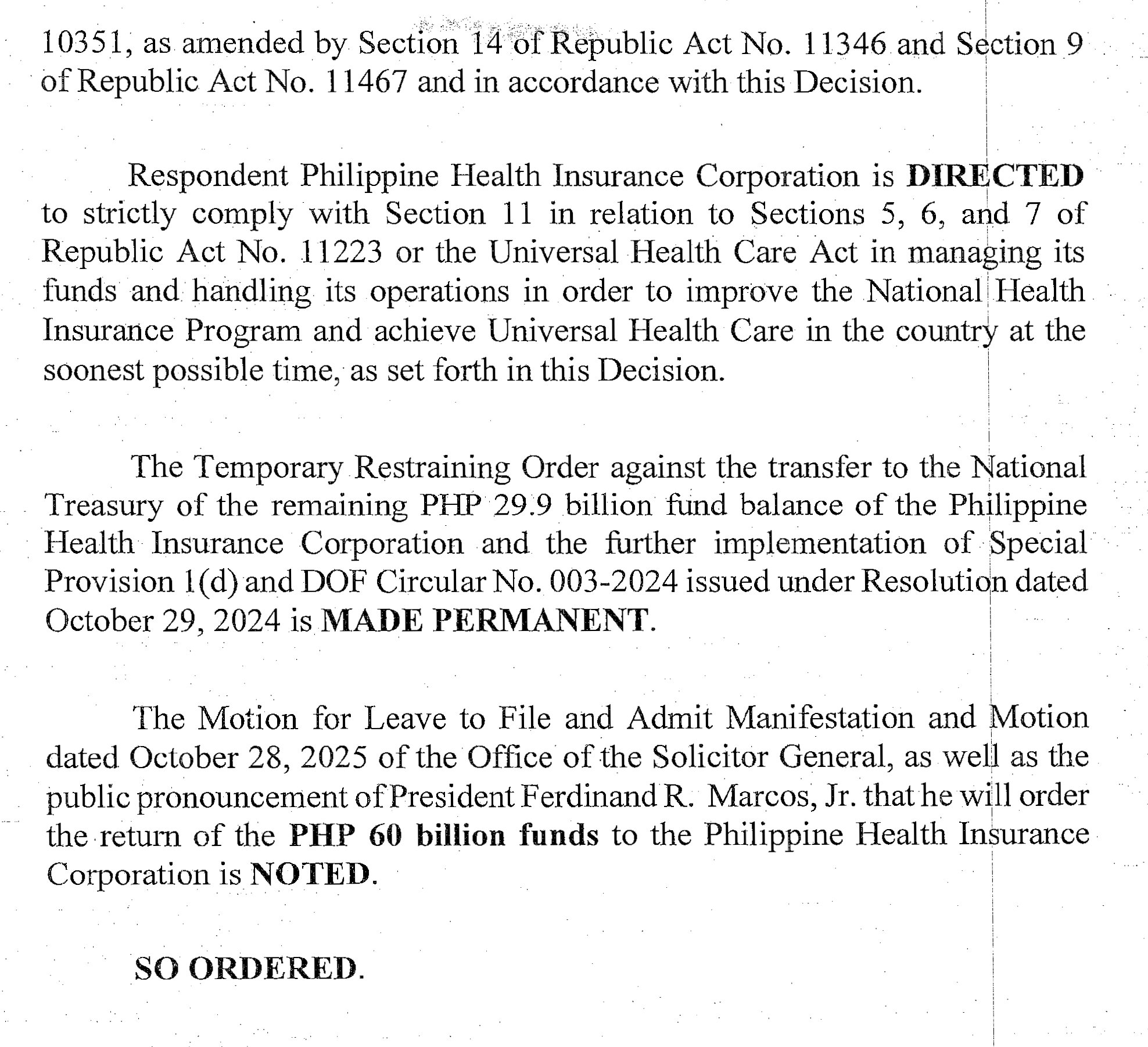

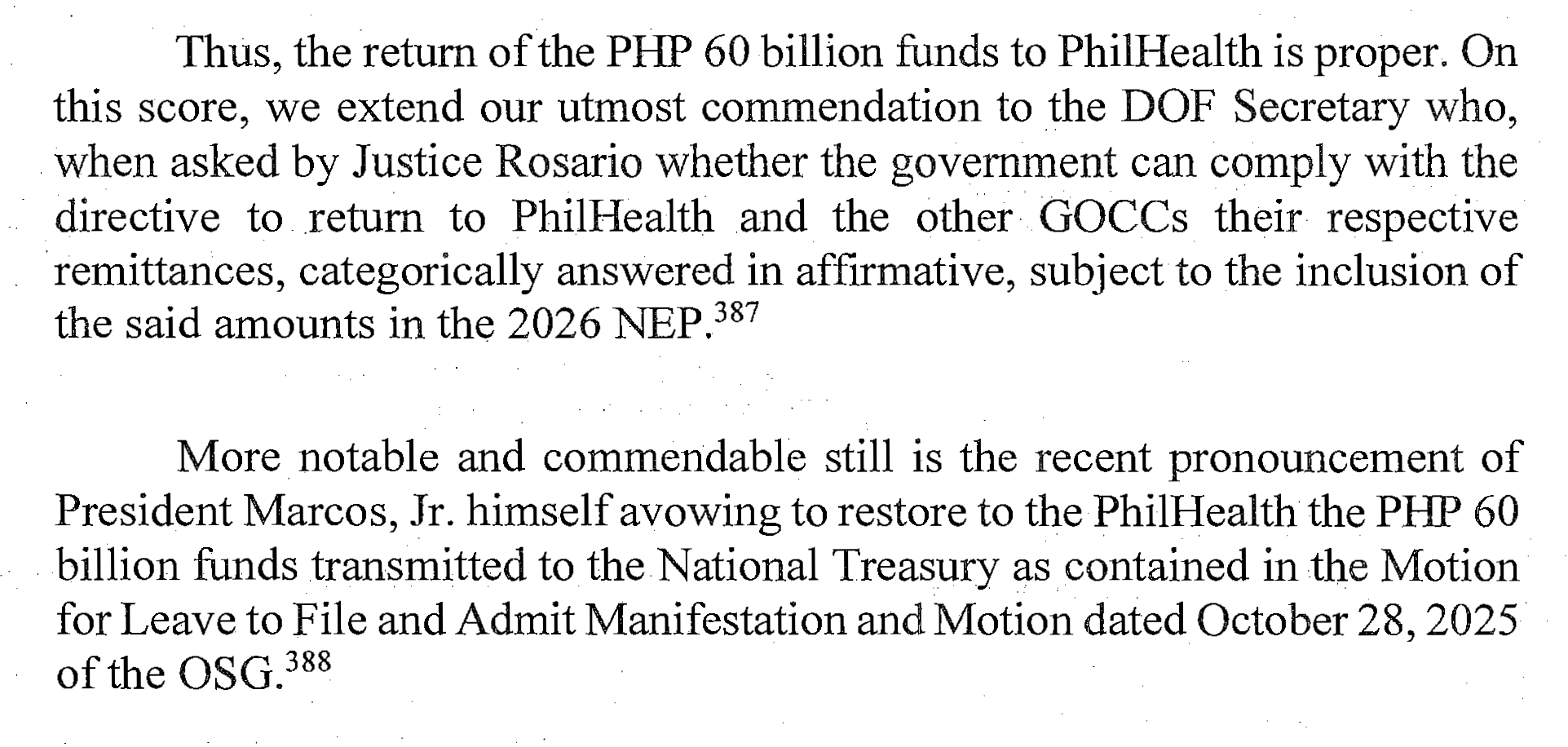

ACCORDINGLY, the Petition for Certiorari is DISMISSED. SO ORDERED.

SUBJECTS/DOCTRINES/DIGEST:

xxxxxxxxxxxxxxxxxxxxxxxxxx

In its findings against petitioner, COMELEC determined that private respondents were not campaign volunteers of petitioner based on several indicators: (i) they were not part of the volunteers’ exclusive group chat; (ii) they were invited only on the day of the event; and (iii) they were excluded from logistical provisions such as meals. The petitioner’s own witness confirmed that the food given to private respondents was merely leftover lunch intended for actual volunteers. These facts led COMELECto conclude that private respondents were mere participants, not volunteers, and that the event was not exclusive to campaign staff, but aimed at securing electoral support.44

Consequently, COMELEC found that the distribution of material considerations, such as red t-shirts and PHP 1,000′.00 cash, was neither documented nor subjected to liquidation, contrary to the petitioner’s claim that these were campaign-related advances. The absence of records, such as logbook entries or receipts, undermined petitioner’s defense and suggested that the funds were given to influence electoral choices … COMELEC emphasized that petitioner’s presence and active participation in the event, including delivering a campaign speech and engaging with private respondents during and after the distribution, demonstrated his knowledge and tacit consent. These acts, coupled with the timing and undocumented nature of the distributions, supported the finding that vote-buying occurred, in violation of Section261(a)(l) of the OEC.

· Evidently, COMELEC laid out a clear. factual. and legal basis for its conclusion. The absence of grave abuse of discretion is manifest where a tribunal adheres to applicable laws, and, anchors· its findings on substantial evidence. Given that COMEEEC’s Resolution was reached through a reasoned evaluation of facts, applicable laws and pertinent jurisprudence, it cannot be said to have acted arbitrarily or capriciously. Consequently, petitioner failed to show that COMELEC committed grave abuse of discretion amounting to lack or excess of jurisdiction in issuing its assailed Resolution.

TO READ THE DECISION, JUST CLICK/DOWNLOAD THE FILE BELOW. IF FILE DOES NOT APPEAR ON SCREEN GO TO DOWNLOAD. IT IS THE FIRST ITEM. OPEN IT.

NOTE: TO RESEARCH ON A TOPIC IN YAHOO OR GOOGLE SEARCH JUST TYPE “attybulao and the topic”. EXAMPLE: TO RESEARCH ON FORUM SHOPPING JUST TYPE “attybulao and forum shopping”.

NOTE: TO RESEARCH ON A TOPIC IN YAHOO OR GOOGLE SEARCH JUST TYPE “attybulao and the topic”. EXAMPLE: TO RESEARCH ON FORUM SHOPPING JUST TYPE “attybulao and forum shopping”.