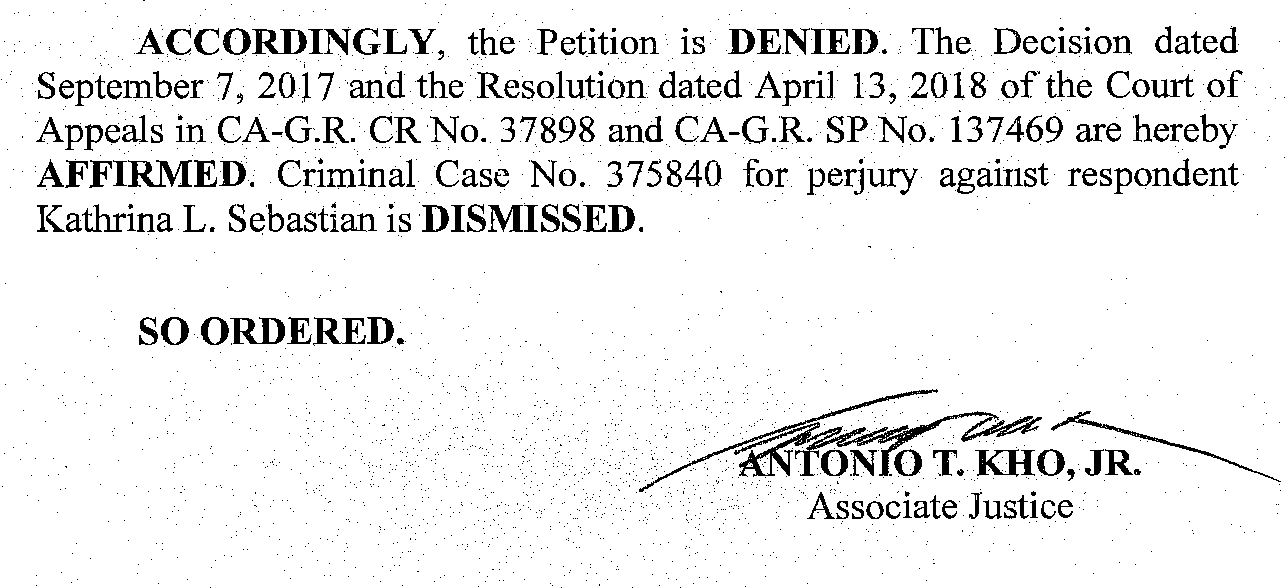

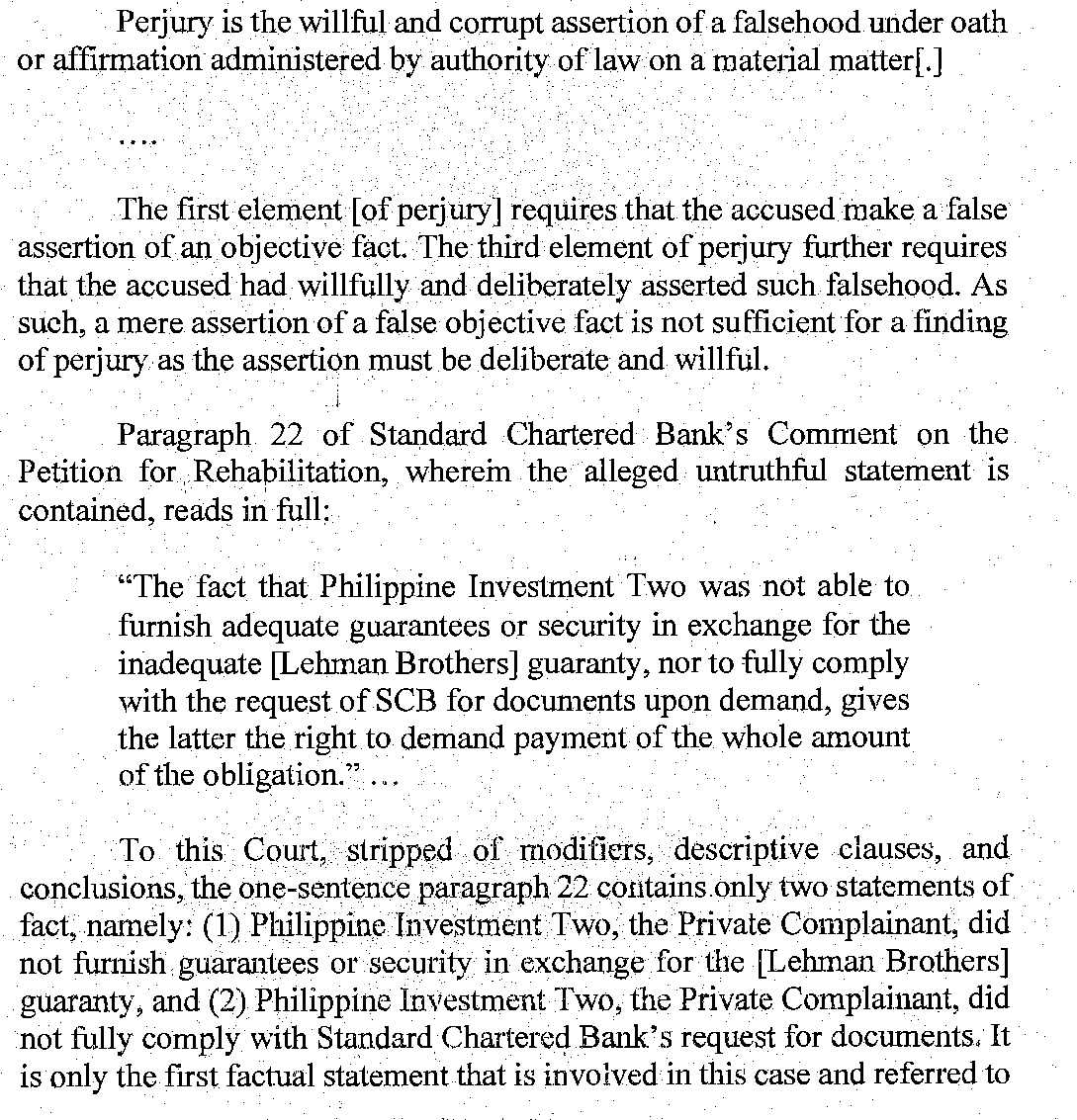

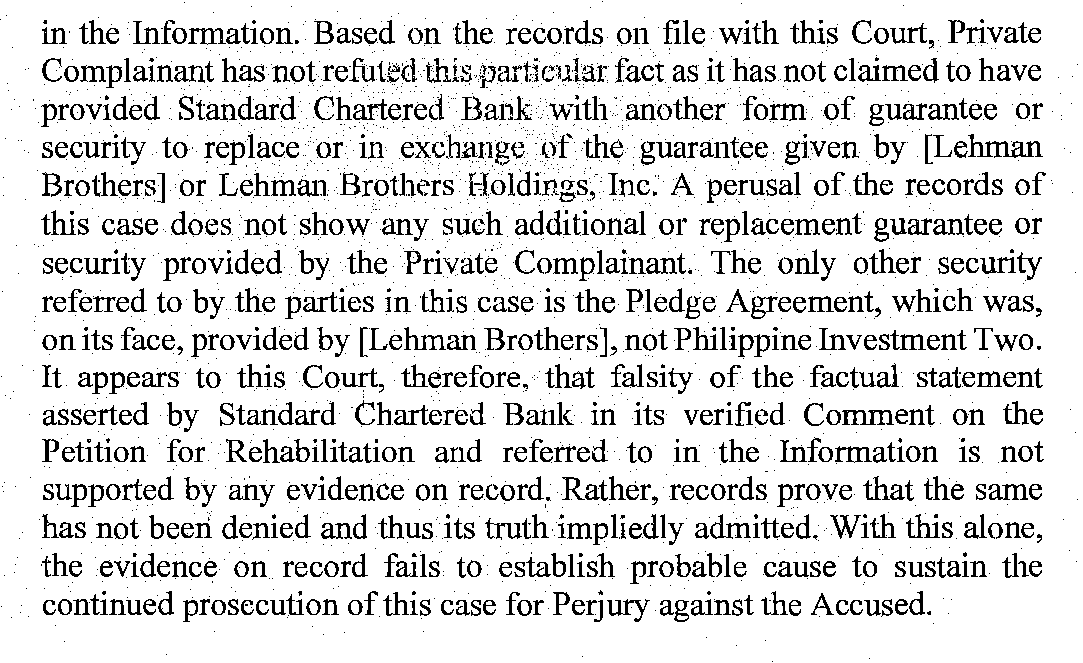

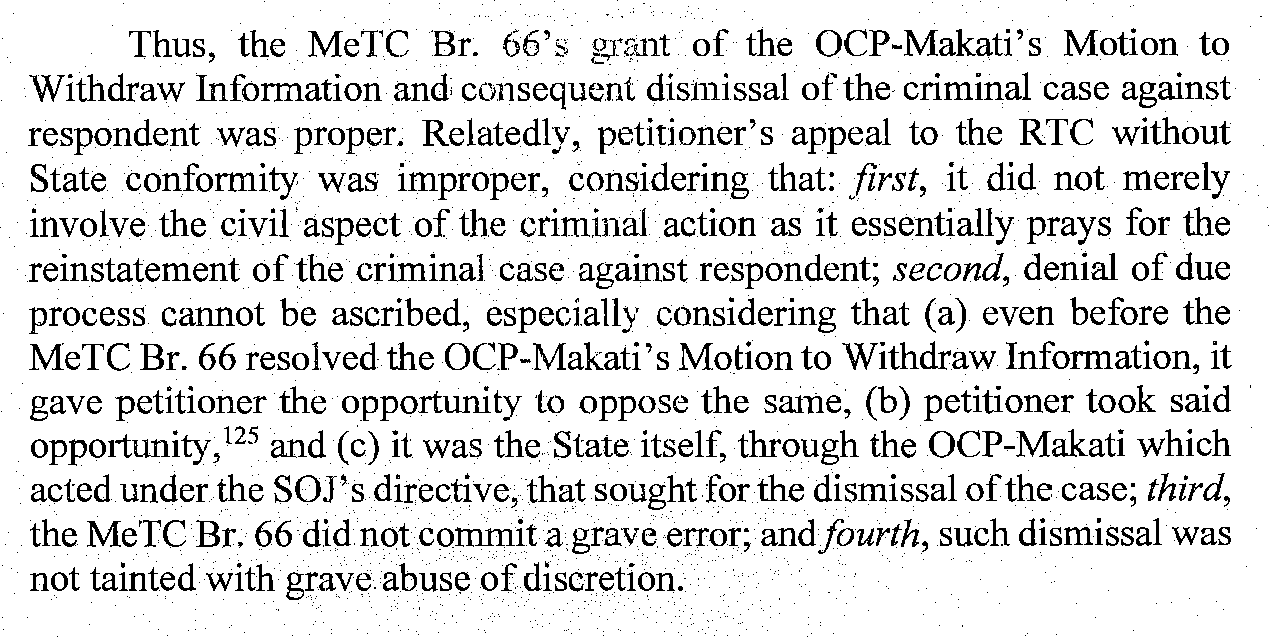

DISPOSITIVE:

ACCORDINGLY, the Petition for Review on Certiorari is

DENIED. The Decision dated July 28, 2021, and the Resolution dated

July 1, 2022, of the Court of Appeals in CA-G.R. CV No. 06914 are

AFFIRMED.

SO ORDERED.

SUBJECTS/DOCTRINES/DIGEST:

FALSE AFFIDAVIT OF COHABITATION RENDERS MARRIAGE VOID.

As the records of this case show, there is inadequate evidence

proving that Alma and Boots continuously and exclusively cohabited as

husband and wife for a period of five years immediately preceding the

celebration of their marriage. At most, the two dated exclusively and

sojourned in several places. However, the fact that they intermittently and

occasionally stayed in the same place does not amount to cohabitation as

husband and wife contemplated by Article 34 of the Family Code. Verily,

Boots admitted signing the Affidavit of Cohabitation despite not meeting

the statutory conditions. Such falsity renders the affidavit ineffectual; it

does not confer exemption from the license requirement. The marriage,

founded on this false declaration, is void.

TO READ THE DECISION, JUST CLICK/DOWNLOAD THE FILE BELOW. IF FILE DOES NOT APPEAR ON SCREEN GO TO DOWNLOAD. IT IS THE FIRST ITEM. OPEN IT.

NOTE: TO RESEARCH ON A TOPIC IN YAHOO OR GOOGLE SEARCH JUST TYPE “attybulao and the topic”. EXAMPLE: TO RESEARCH ON FORUM SHOPPING JUST TYPE “attybulao and forum shopping”.